State Pension Tax Raid Explained: Why More Retirees Could Pay Income Tax?

The phrase state pension tax raid describes the growing likelihood that more UK pensioners will pay income tax as the State Pension rises under the Triple Lock while the Personal Allowance remains frozen at £12,570.

It is not a new or separate tax, but the effect of fiscal drag gradually drawing more retirees into the tax system.

Key answer points:

- It refers to rising State Pension payments combined with frozen tax thresholds increasing tax liability.

- The Triple Lock raises pensions annually by inflation, earnings growth or 2.5 percent, whichever is highest.

- The frozen Personal Allowance means more pension income becomes taxable over time.

- Income tax applies when total annual income exceeds £12,570.

- The debate centres on fairness, transparency and long term fiscal sustainability.

What Is the “State Pension Tax Raid” and Why Is Everyone Talking About It?

The term state pension tax raid has gained traction across UK media, political debates and financial commentary. It is important to clarify from the outset that this is not the name of an official government policy.

There is no specific legislation titled “State Pension Tax Raid”. Instead, the phrase is widely used to describe a financial effect that is gradually bringing more pensioners into the income tax system.

At its core, the debate centres on a simple reality. The State Pension is rising each year under the Triple Lock, while the Personal Allowance remains frozen at £12,570.

As pension income increases but the tax free threshold stays the same, more retirees risk exceeding the limit at which income tax becomes payable.

The State Pension has always been taxable income. That fact is not new. What is new is the growing proximity between the full new State Pension and the tax free Personal Allowance.

When people hear the phrase state pension tax raid, it often reflects concern that pensioners are being drawn into taxation quietly, without headline changes to tax rates.

To understand why this discussion has intensified, it helps to examine three factors working together:

- The Triple Lock formula

- The freeze on tax thresholds

- Inflation and wage growth

Each of these elements is legitimate policy in its own right. However, their combined impact is reshaping the tax landscape for UK retirees.

Why Is the State Pension Tax Raid Happening Now?

The reason this issue feels urgent is timing. In recent years, inflation has been high and earnings growth has accelerated. Because of the Triple Lock, those factors directly feed into State Pension increases.

How Does the Triple Lock Increase the State Pension?

The Triple Lock guarantees that the State Pension rises annually by the highest of inflation, average earnings growth, or 2.5 percent.

This policy was introduced in 2010 with the aim of protecting pensioners from falling behind the working population.

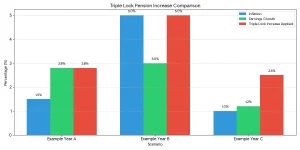

The effect of the Triple Lock can be illustrated clearly.

| Year | Inflation | Earnings Growth | Triple Lock Increase Applied |

| Example Year A | 1.5% | 2.8% | 2.8% |

| Example Year B | 5% | 3% | 5% |

| Example Year C | 1% | 1.2% | 2.5% |

In periods of high inflation or strong wage growth, pension increases can be significant. Over time, these rises compound. This is why the full new State Pension has climbed steadily and is now close to the £12,570 Personal Allowance threshold.

What Role Does the Personal Allowance Freeze Play?

While pensions have increased, the Personal Allowance has remained frozen at £12,570 since April 2021. It is expected to remain at that level until at least 2028.

Freezing thresholds during periods of rising incomes increases the number of people who pay tax. This is known as fiscal drag.

A senior government finance professional explained the mechanism clearly during a policy discussion:

“The State Pension has always been taxable income. There is no new pension tax being introduced. What is happening is that the Personal Allowance is frozen. When incomes rise due to the Triple Lock and thresholds remain static, more individuals become liable for income tax. That outcome is a function of fiscal policy rather than a targeted measure against pensioners.”

This distinction is crucial. There is no new standalone pension tax. Instead, the structure of existing policy produces the effect.

How Does Fiscal Drag Quietly Increase Tax Bills?

Fiscal drag operates without increasing tax rates. It simply allows inflation and income growth to move people into taxable territory.

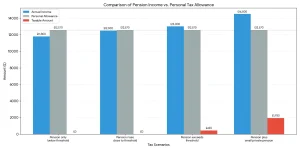

Consider the following simplified comparison.

| Scenario | Annual Income | Personal Allowance | Taxable Amount |

| Pension only below threshold | £11,800 | £12,570 | £0 |

| Pension rises close to threshold | £12,500 | £12,570 | £0 |

| Pension exceeds threshold | £13,000 | £12,570 | £430 |

| Pension plus small private pension | £14,500 | £12,570 | £1,930 |

The table shows how even modest increases can create taxable income.

For many pensioners, the shift may be small initially. However, the psychological impact can be significant. Individuals who have never paid tax in retirement may suddenly receive a notice from HMRC.

Will Pensioners Really Pay Income Tax on the State Pension?

The straightforward answer is yes, but only if total taxable income exceeds the Personal Allowance.

The State Pension counts as taxable income. However, it is paid without tax deducted at source. This means any tax due is typically collected through adjustments to other income streams such as private pensions.

To understand the mechanics, it helps to break down the components of retirement income.

| Income Source | Taxable Status | Tax Deducted Automatically |

| State Pension | Taxable | No |

| Private Pension | Taxable | Yes via PAYE |

| Part time Employment | Taxable | Yes via PAYE |

| Savings Interest | Taxable above allowance | No automatic PAYE |

If a pensioner receives only the State Pension and it remains below £12,570, no income tax is payable. However, many retirees also receive:

- Occupational pensions

- Personal pensions

- Part time earnings

- Rental income

- Investment returns

Even a modest private pension can push total income above the threshold.

When Does a Retiree Actually Cross the Tax Threshold?

Let us look at a realistic scenario.

| Component | Annual Amount |

| State Pension | £11,800 |

| Small Private Pension | £2,500 |

| Total Income | £14,300 |

| Personal Allowance | £12,570 |

| Taxable Income | £1,730 |

In this example, the retiree pays income tax on £1,730. At a basic rate of 20 percent, that equates to £346 in tax.

For some, that may seem manageable. For others living on tight budgets, it is meaningful.

Many pensioners are unaware that the State Pension is taxable. Because no tax is deducted directly from it, there can be confusion about how liabilities arise.

How Does the State Pension Tax Raid Affect Real People in Practice?

To understand how the state pension tax raid works in real life, consider a practical example of a typical UK retiree.

Margaret is 68 and receives the full new State Pension. Her annual State Pension income is £11,900. She also has a small workplace pension that pays her £3,000 per year.

Her total annual income looks like this:

| Income Source | Annual Amount |

| State Pension | £11,900 |

| Workplace Pension | £3,000 |

| Total Income | £14,900 |

| Personal Allowance | £12,570 |

| Taxable Income | £2,330 |

Margaret’s taxable income is £2,330. At the basic rate of 20 percent, she pays £466 in income tax for the year.

Importantly, no tax is deducted directly from her State Pension. Instead, HMRC adjusts the tax code on her workplace pension so that the correct tax is collected through PAYE.

Now imagine the State Pension increases again under the Triple Lock to £12,500. If her workplace pension remains £3,000, her new position would be:

| Income Source | Annual Amount |

| State Pension | £12,500 |

| Workplace Pension | £3,000 |

| Total Income | £15,500 |

| Personal Allowance | £12,570 |

| Taxable Income | £2,930 |

Her taxable income rises to £2,930, increasing her annual tax bill.

This example shows that the issue is not about a sudden new tax being introduced. Instead, gradual pension increases combined with a frozen Personal Allowance steadily increase taxable income. For retirees with even modest additional pensions, the effect becomes more noticeable each year.

How Close Is the Full New State Pension to the Tax Free Personal Allowance?

The narrowing gap between the State Pension and the Personal Allowance is central to the debate.

If current growth trends continue, it is feasible that the full new State Pension could exceed £12,570 in the coming years. Should that happen, even pensioners with no additional income could become income taxpayers.

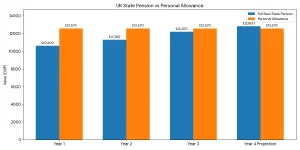

The relationship between pension growth and threshold freeze can be illustrated as follows.

| Year | Full New State Pension | Personal Allowance | Difference |

| Year 1 | £10,600 | £12,570 | £1,970 |

| Year 2 | £11,300 | £12,570 | £1,270 |

| Year 3 | £12,200 | £12,570 | £370 |

| Year 4 Projection | £12,800 | £12,570 | £230 over |

This table shows how gradual increases can eventually eliminate the buffer between pension income and tax liability.

Once the pension exceeds the allowance, even those without private pensions may pay basic rate income tax on the excess.

Why Is the State Pension Tax Raid Politically Sensitive?

The issue is politically charged because it intersects with promises of pension protection.

The Triple Lock was introduced to ensure that pensioners did not fall behind in living standards. At the same time, frozen tax thresholds increase tax revenue without altering tax rates.

Critics describe this as a stealth tax. Supporters argue that freezing thresholds is necessary to stabilise public finances after periods of economic strain.

From my own analysis as a financial writer, I see both sides. I often explain to readers that the mechanics are structural rather than punitive.

At the same time, I understand why many retirees feel unsettled when they learn that their State Pension is taxable.

“I believe much of the confusion stems from communication. When pensioners hear about rising State Pension payments, they assume it is entirely beneficial. Few immediately consider how frozen thresholds interact with those increases. Greater transparency would help reduce the sense of surprise.”

Political sensitivity also arises because pensioners represent a significant voting demographic. Any perception of reduced benefits or increased taxation can become a focal point during Budget announcements and general elections.

Is the State Pension Tax Raid a New Government Policy?

No new policy has been introduced that specifically taxes the State Pension. The taxation rules have not fundamentally changed. The State Pension has long been classified as taxable income.

The change lies in the interaction of existing policies:

- The Triple Lock increases pension payments

- The freeze on the Personal Allowance

- Broader economic inflation

A government finance professional summarised it succinctly:

“There is no line in the Budget that says we are introducing a State Pension tax. The structure has been in place for years. What has shifted is the economic environment. When earnings and pensions grow but allowances remain static, more people enter the tax system. That is how fiscal drag works.”

Understanding this distinction is critical for balanced analysis. The phrase state pension tax raid reflects political framing rather than legislative change.

What Should Pensioners Do If They Are Concerned About Paying Tax?

Planning and awareness are essential. Retirees should review their total income each year and consider how different income sources combine.

Key actions may include:

- Checking total annual income from all sources

- Reviewing HMRC tax codes

- Monitoring private pension withdrawals

- Assessing savings interest levels

For those nearing retirement, it may also be beneficial to examine how different withdrawal strategies affect tax exposure.

For example, spreading withdrawals across tax years or coordinating private pension drawdown with State Pension timing can help manage liability.

Seeking independent financial advice can be valuable, particularly for individuals with multiple income streams or investments.

Is the Triple Lock Sustainable in the Long Term?

The sustainability of the Triple Lock is frequently debated in economic circles.

On one hand, it has successfully increased pension incomes and reduced pensioner poverty. On the other, it creates long term fiscal commitments that grow with inflation and earnings.

If the State Pension continues to rise faster than tax thresholds, more pensioners may enter the tax system. This could partially offset the cost of increases, but it may also intensify public debate.

The Treasury faces competing priorities:

- Managing national debt

- Funding public services

- Supporting an ageing population

Any future reform to the Triple Lock or the Personal Allowance would significantly alter the state pension tax raid discussion.

For now, the structure remains unchanged. Pensioners should focus on understanding how their income interacts with the tax system rather than relying solely on political narratives.

In practical terms, the situation is not about a sudden new tax. It is about the gradual convergence of pension income and frozen tax thresholds. As that convergence continues, awareness and proactive financial planning become increasingly important for UK retirees.

Conclusion: Is the “State Pension Tax Raid” a Reality or a Political Label?

The “state pension tax raid” is not an official tax policy. It describes the growing likelihood that more pensioners will pay income tax because the State Pension is rising while the Personal Allowance remains frozen.

Whether you see it as a stealth tax or simply fiscal drag depends on perspective. What is clear is that the State Pension has always been taxable income, and retirees should understand how total income affects their tax position.

As pension payments continue to rise under the Triple Lock, awareness and planning will become increasingly important for UK retirees.

Frequently Asked Questions About the State Pension Tax Raid

Does everyone receiving the State Pension pay income tax?

No. You only pay income tax if your total taxable income exceeds the Personal Allowance of £12,570.

Why is tax not deducted directly from the State Pension?

The State Pension is paid without PAYE deductions. Any tax owed is usually collected through other income sources or via HMRC adjustments.

Could the Personal Allowance increase in future?

Yes, future governments may choose to raise it, but it is currently frozen until at least 2028.

What happens if I underpay tax on my pension income?

HMRC may adjust your tax code or issue a calculation requiring repayment.

Is the basic State Pension also taxable?

Yes. Both the basic and new State Pension count as taxable income.

How does savings interest affect pension tax?

Interest above your Personal Savings Allowance counts towards taxable income and may push you over the threshold.

Will the State Pension eventually exceed the tax-free allowance?

If the Triple Lock continues and the Personal Allowance remains frozen, it is possible in future years.

What is your reaction?