How Much is the State Pension for a Woman?

The State Pension for a woman in the UK is the same as for men and depends mainly on National Insurance contributions. For the 2025/26 tax year, the full new State Pension is £230.25 per week, which is about £11,973 per year, provided a woman has 35 qualifying years of National Insurance contributions.

Women with 10 to 34 qualifying years receive a reduced amount, while those under the older basic State Pension system may receive up to £176.45 per week. The State Pension age is currently 66, and payments are expected to increase slightly each year due to the government’s triple lock policy.

Key Takeaways

- Full new State Pension for 2025/26 is £230.25 per week

- Women need 35 National Insurance qualifying years for the full pension

- Minimum 10 qualifying years required to receive any State PensionBasic State

- Pension under the older system is £176.45 per week

- State Pension age in the UK is currently 66 for both men and women

- Payments may increase annually through the triple lock policy

- Future projections suggest the pension could rise to around £241.30 per week from April 2026

What Is the Current State Pension Amount for a Woman in the UK?

The State Pension in the United Kingdom is a regular payment from the government that individuals receive once they reach the State Pension age.

The amount a woman receives depends mainly on her National Insurance contribution record and whether she falls under the new State Pension system or the older basic State Pension system.

In the modern UK pension system, men and women receive the same State Pension amount. The government removed gender differences in pension payments and retirement age over time, creating a unified structure where eligibility and payment levels are determined primarily by contribution history.

Women who reached State Pension age on or after 6 April 2016 usually fall under the new State Pension system. Those who reached State Pension age before this date are generally part of the older basic State Pension structure.

Full New State Pension (2025/26 Tax Year)

For the 2025/26 tax year, the full new State Pension is £230.25 per week. This equates to approximately £997 per month or around £11,973 per year.

To receive the full amount, a woman normally needs 35 qualifying years of National Insurance contributions or credits. Qualifying years are typically built through employment, self-employment, or by receiving National Insurance credits during periods such as childcare or caring responsibilities.

If a woman has fewer than 35 years but at least 10 qualifying years, she can still receive a portion of the pension. The payment will be calculated proportionally based on the number of qualifying years she has accumulated.

Key facts about the new State Pension include:

- Full weekly payment of £230.25 in the 2025/26 tax year

- A minimum of 10 qualifying years is required to receive any pension

- 35 qualifying years are usually required to receive the full amount

- Payments are made every four weeks into a bank account

The following table shows the approximate pension amounts based on qualifying years.

| Qualifying Years | Estimated Weekly Pension | Estimated Annual Pension |

| 35 years | £230.25 | £11,973 |

| 30 years | About £197 | About £10,244 |

| 25 years | About £164 | About £8,528 |

| 20 years | About £131 | About £6,812 |

| 10 years | About £66 | About £3,432 |

The proportional system means that every qualifying year contributes to the final pension amount.

Basic State Pension for Women Under the Old System

Women who reached State Pension age before the introduction of the new system usually receive the basic State Pension. For the 2025/26 tax year, the full basic State Pension is £176.45 per week.

Under this system, women generally needed around 30 qualifying years of National Insurance contributions to receive the full basic pension amount.

Some individuals under the old system may also receive additional pension payments depending on their work history. These additional payments could come from schemes such as the State Earnings Related Pension Scheme or the State Second Pension.

The table below compares the two main pension systems.

| Pension System | Weekly Full Payment | Typical Qualifying Years | Eligibility |

| New State Pension | £230.25 | 35 years | Reached pension age after April 2016 |

| Basic State Pension | £176.45 | 30 years | Reached pension age before April 2016 |

Many pension specialists explain that the new system was introduced to simplify pension rules and create a clearer link between National Insurance contributions and pension entitlement.

A pensions adviser once explained the system clearly by saying,

“Many people assume the State Pension is fixed, but in reality it reflects a lifetime of contributions. Understanding your National Insurance record is one of the most important steps when planning retirement.”

Is the State Pension Different for Women Compared to Men?

In the past, the UK pension system treated men and women differently. Women were allowed to claim State Pension earlier than men and some rules allowed married women to rely partly on their spouse’s National Insurance contributions.

Over time, the government introduced several reforms to create a more equal system. Today the State Pension payment is the same for men and women.

The amount someone receives now depends on three main factors:

- The number of qualifying National Insurance years

- The pension system they fall under

- Any additional pension entitlements from older schemes

Gender no longer influences the weekly pension payment. A woman and a man with identical contribution histories will receive the same State Pension amount.

The following table highlights the historical differences compared to the modern system.

| Feature | Older System | Current System |

| Pension age for women | Earlier than men | Same as men |

| Pension calculation | Some spouse based benefits | Individual contribution based |

| Weekly pension amount | Could differ in some situations | Same for men and women |

The removal of gender based differences has simplified pension planning. Women today build their State Pension entitlement through their own employment, self-employment, and National Insurance credits.

How Much Will the UK State Pension Increase in 2026?

State Pension payments normally increase each year in April. The increase is determined by a policy known as the triple lock.

The triple lock ensures that pensions increase by the highest of three measures:

- Inflation

- Average wage growth

- 2.5 percent

This policy helps protect pensioners from losing purchasing power as living costs rise.

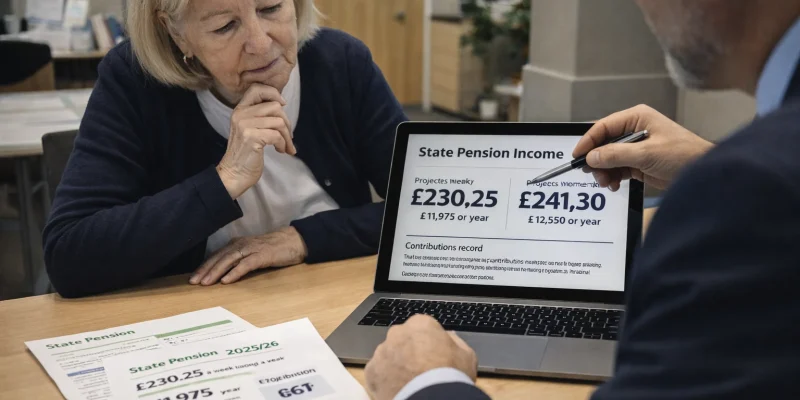

Expected New State Pension Rate from April 2026

Based on current projections, the full new State Pension could increase to around £241.30 per week from April 2026. This would bring the annual pension to roughly £12,548.

The basic State Pension could increase to about £184.90 per week.

The table below compares the current and expected pension amounts.

| Pension Type | 2025/26 Weekly Rate | Estimated 2026 Weekly Rate | Estimated Annual Value 2026 |

| New State Pension | £230.25 | £241.30 | About £12,548 |

| Basic State Pension | £176.45 | £184.90 | About £9,614 |

These increases can significantly affect retirement income over time.

How the Triple Lock Affects Pension Payments?

The triple lock mechanism was introduced to ensure that pension payments keep pace with economic conditions.

A pensions policy analyst once noted,

“The triple lock has played a significant role in improving pension income stability for millions of retirees across the UK.”

From an author perspective, it is clear that the triple lock has become a key factor in retirement planning.

“When researching pension policies, I often notice that many people underestimate how important the annual increase can be. Over a decade of retirement, even small yearly increases can add thousands of pounds to total pension income.”

How Many National Insurance Years Does a Woman Need for the Full State Pension?

National Insurance contributions are the main factor used to determine State Pension eligibility. Each year in which a person pays or receives National Insurance credits usually counts as a qualifying year.

Minimum Qualifying Years

Under the new State Pension rules, at least 10 qualifying years are required to receive any State Pension. To receive the full pension amount, a person typically needs 35 qualifying years.

Qualifying years can be built in several ways:

- Working and paying National Insurance contributions

- Being self-employed and paying the appropriate contributions

- Receiving National Insurance credits while caring for children

- Receiving certain benefits that provide contribution credits

The following table illustrates how contribution years influence pension entitlement.

| Contribution Years | Pension Eligibility |

| Less than 10 years | Usually no State Pension |

| 10 to 34 years | Partial pension |

| 35 years or more | Full new State Pension |

This system encourages consistent contributions throughout a working career.

How do reduced National Insurance Contributions Affect Women?

In the past, some married women paid reduced-rate National Insurance contributions. This arrangement was commonly called the married woman’s stamp.

The scheme allowed married women to pay lower contributions, but it also meant they built little or no entitlement to their own State Pension.

The scheme ended in April 1977, but its impact still affects some older pensioners today.

Women who paid reduced contributions may experience situations such as:

- Lower personal State Pension entitlement

- Eligibility for pension based on a spouse’s contributions

- Dependence on older pension rules

A pension adviser once commented,

“Many women who paid the married woman’s stamp were unaware of how it would affect their retirement income decades later.”

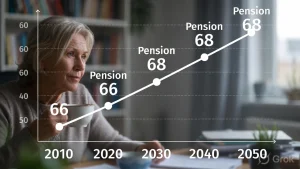

What Is the State Pension Age for Women in the UK?

The State Pension age is the age at which individuals can begin receiving their government pension payments.

Currently, the State Pension age in the UK is 66 for both men and women.

Historically, women could claim the State Pension at age 60 while men claimed at 65. The government gradually increased the pension age for women to align it with that of men.

Future increases are also planned as life expectancy rises.

The table below summarises the expected timeline for pension age changes.

| Time Period | State Pension Age |

| Current | 66 |

| Between 2026 and 2028 | Gradual rise to 67 |

| Future proposals | Possible increase to 68 |

These changes aim to ensure the sustainability of the State Pension system as people live longer and spend more years in retirement.

How Is the State Pension Calculated for Women?

The calculation of State Pension payments is based mainly on National Insurance contribution records. Each qualifying year adds value to the overall pension entitlement.

National Insurance Contribution Records

National Insurance records track contributions made throughout a person’s working life.

Qualifying years can come from several sources:

- Employment contributions through payroll

- Self-employment contributions

- Credits awarded during periods of childcare

- Credits provided while caring for disabled relatives

The government keeps an official record of these contributions, which determines how much pension someone will receive.

Partial Pension Calculations

If a woman has fewer than 35 qualifying years, the pension amount is calculated proportionally.

For example, if a person has accumulated 20 qualifying years, they may receive approximately 20 divided by 35 of the full State Pension.

The table below demonstrates how partial pension calculations work.

| Qualifying Years | Portion of Full Pension | Estimated Weekly Pension |

| 35 years | 100 percent | £230.25 |

| 28 years | 80 percent | About £184 |

| 21 years | 60 percent | About £138 |

| 14 years | 40 percent | About £92 |

“I often explain to readers that even small gaps in National Insurance records can reduce pension income. Checking your contribution history early can make a meaningful difference to your retirement planning.”

What Happens If a Woman Does Not Have 35 Years of National Insurance?

A woman with fewer than 35 qualifying years will normally receive a reduced State Pension. However, there are ways to improve pension entitlement before reaching retirement age.

One common option is making voluntary National Insurance contributions. These payments allow individuals to fill gaps in their contribution history.

Voluntary contributions may be helpful if someone has:

- Periods of unemployment without credits

- Years spent living abroad

- Career breaks that did not qualify for National Insurance credits

Another option is continuing to work for additional years to accumulate more qualifying contributions.

Financial advisers often emphasise the importance of reviewing pension forecasts early.

A retirement planning specialist explained the importance of this step by saying,

“Many people only look at their State Pension shortly before retirement. Checking it years in advance gives you time to increase your qualifying years and potentially improve your pension income.”

Can Married Women Claim State Pension Based on Their Spouse’s Record?

In certain circumstances, married women may be able to receive State Pension benefits based on their spouse’s National Insurance contributions. These rules mainly apply to individuals under the older basic State Pension system.

For example, a married woman may receive up to 60 percent of her husband’s basic State Pension if she has limited qualifying contributions of her own.

Widows may also inherit certain pension rights depending on their spouse’s contribution record.

These provisions were designed to support households where one partner had limited employment history.

However, under the newer State Pension system introduced in 2016, entitlement is generally based on an individual’s own National Insurance contributions rather than those of a spouse.

How Can a Woman Check Her State Pension Forecast?

The UK government provides an official State Pension forecast service that allows individuals to see an estimate of their future pension payments.

The forecast provides several key details:

- Estimated weekly pension amount

- Current number of qualifying National Insurance years

- Remaining years required to reach the full pension

- Official State Pension age

Reviewing this information can help people make informed financial decisions about their retirement.

“I often recommend that people check their State Pension forecast as early as possible. It provides a clear picture of future income and helps identify whether voluntary contributions might increase pension payments.”

What Other Benefits Can Women Receive Alongside the State Pension?

The State Pension may not be the only financial support available during retirement. Some individuals may qualify for additional government benefits designed to support older residents.

Pension Credit

Pension Credit is designed to help retirees with lower incomes. It provides additional weekly payments and can also give access to other financial support schemes.

Winter Fuel Payment

Winter Fuel Payments help older individuals cover heating costs during colder months. These payments are typically provided automatically to eligible pensioners.

Additional Government Support

Some pensioners may also qualify for other support programmes depending on their income and circumstances.

Examples include:

- Council tax support

- Cost of living payments

- Free TV licences for certain age groups

These programmes can provide additional financial stability and improve overall retirement income for many households.

Conclusion: How Much Is the State Pension for a Woman in the UK?

The State Pension for a woman in the UK depends mainly on National Insurance contributions and the pension system she falls under.

For the 2025/26 tax year, the full new State Pension is £230.25 per week, provided a woman has 35 qualifying years of National Insurance contributions. Those with fewer years receive a reduced amount, while women under the older basic State Pension system may receive up to £176.45 per week.

From April 2026, the full new State Pension is expected to rise to around £241.30 per week, reflecting annual increases under the triple lock policy.

Understanding the rules around qualifying years, pension age, and contribution records can help women better prepare for retirement and maximise the pension income they receive.

FAQs

Can a woman receive State Pension without National Insurance contributions?

A woman generally needs at least 10 qualifying years of National Insurance contributions or credits to receive any State Pension. Without these contributions, entitlement is usually not possible.

Do women get the same State Pension as men in the UK?

Yes. The UK State Pension system now provides equal payments for men and women. The amount depends on National Insurance records rather than gender.

Can a woman increase her State Pension before retirement?

Yes. Some women can increase their pension by paying voluntary National Insurance contributions to fill gaps in their contribution history.

What happens if a woman delays claiming her State Pension?

If someone delays claiming their State Pension, the amount may increase slightly for each additional week of delay.

Do married women automatically receive their husband’s pension?

No. Under the modern system, pensions are mainly based on individual contributions, although some older rules allow limited claims based on a spouse’s record.

How often does the UK State Pension increase?

The State Pension usually increases every year in April, based on the triple lock system.

Is the State Pension taxable in the UK?

Yes. The State Pension counts as taxable income, although tax is only payable if total income exceeds the personal allowance threshold.

What is your reaction?