Noncum Tax Code UK: Understanding Non-Cumulative Tax Codes

Last Updated On – 27-05-2026

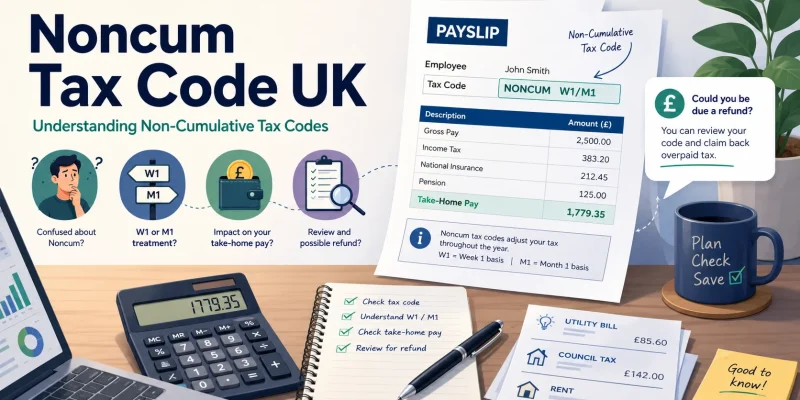

A noncum tax code means income tax is calculated only on the current pay period, not on the employee’s total income for the tax year so far.

In the UK, it is often shown as W1, M1, or sometimes linked with emergency tax. It is usually temporary and commonly appears when HMRC or payroll does not yet have full income details.

Key takeaways:

- A noncum tax code means each payday is treated separately.

- Unused personal allowance from earlier months or weeks is not carried forward.

- It may cause temporary overpayment of tax.

- Common reasons include starting a new job, missing P45, second jobs, or pension income.

- Employees can fix it by giving payroll the right documents or updating details with HMRC.

What Does a Noncum Tax Code Mean in the UK?

A noncum tax code means the payroll system calculates tax based only on what someone earns in one pay period.

It does not take account of previous earnings, earlier tax deductions, or unused tax-free allowance from earlier weeks or months in the same tax year.

Under the PAYE system, most employees are given a tax code by HMRC. This code tells the employer how much tax-free income the employee can receive before income tax is deducted.

A standard tax code is usually cumulative, meaning it looks at the employee’s total income and tax position from the start of the tax year.

A non-cumulative code works differently. It treats each pay period as separate.

Non-Cumulative Tax Code Meaning

A non-cumulative tax code does not “look back” at earlier pay periods. This means the payroll system will not check whether the employee has unused personal allowance from previous weeks or months.

For example, if someone did not work for the first two months of the tax year and then started a job, a cumulative code may allow the unused personal allowance from those earlier months to be used.

A non-cumulative code will not do this. It only gives the allowance for the current pay period.

How W1 and M1 Tax Codes Work?

A non-cumulative code is often marked as:

- W1 for weekly payroll

- M1 for monthly payroll

- X in some payroll systems to show emergency or non-cumulative treatment

These codes tell the employer to tax the person on a week-by-week or month-by-month basis. The calculation does not adjust automatically for tax already paid or unpaid earlier in the year.

How Does a Noncum Tax Code Affect PAYE Income Tax?

A noncum tax code affects PAYE by limiting the tax calculation to the current wage or salary payment. It can be useful as a temporary measure, but it may not give the most accurate tax result over the full tax year.

PAYE is designed to collect income tax gradually from wages, salaries, pensions, and some other taxable income.

When the correct cumulative code is used, PAYE aims to balance a person’s tax position throughout the year. A non-cumulative code does not provide the same balancing effect.

Pay-Period-Only Tax Calculation

With a non-cumulative code, the employer calculates tax as though the current week or month stands alone. The system does not review the employee’s full annual tax position.

This can be helpful when HMRC does not yet know the person’s full employment history. However, it can also mean that someone pays more tax in the short term.

For example, an employee who starts work halfway through the tax year may have unused personal allowance from earlier months. A cumulative tax code could take that into account. A non-cumulative tax code will usually ignore it until the code is corrected.

No Rollover of Unused Personal Allowance

The UK personal allowance is the amount of income most people can earn before paying income tax. When a tax code is cumulative, unused allowance can build up and be used later in the tax year.

With a non-cumulative code, unused allowance does not roll forward. Each week or month is calculated separately, which can make the tax deduction appear higher than expected.

A payroll adviser explained this common issue clearly:

“I often see employees panic when they notice M1 or W1 on their payslip. In many cases, I tell them it does not always mean anything is wrong permanently. It usually means payroll has been told to tax this pay period on its own until HMRC confirms the full details.”

What Is the Difference Between a Cumulative and Non-Cumulative Tax Code?

The main difference is that a cumulative tax code considers the full tax year so far, while a non-cumulative tax code only considers the current pay period.

This distinction is important because it affects whether the payroll system can correct overpayments or underpayments during the year.

| Feature | Cumulative Tax Code | Non-Cumulative Tax Code |

| Tax calculation | Based on total income and tax paid in the tax year so far | Based only on the current pay period |

| Personal allowance | Unused allowance can roll forward | Unused allowance does not roll forward |

| Common code style | 1257L, depending on circumstances | 1257L W1, 1257L M1, or emergency code |

| PAYE adjustment | Can correct overpaid or underpaid tax during the year | Usually does not correct earlier periods automatically |

| Common use | Standard ongoing employment | New job, missing P45, emergency tax, incomplete HMRC records |

Cumulative Tax Code Explained

A cumulative tax code works by spreading a person’s tax-free allowance across the tax year. It checks how much the person has earned since 6 April, how much tax has already been deducted, and how much allowance has been used.

This allows PAYE to make adjustments. If someone paid too much tax earlier in the year, a cumulative code may reduce tax in a later pay period. If someone paid too little, it may increase deductions gradually.

Non-Cumulative Tax Code Explained

A non-cumulative tax code does not carry out this year-to-date balancing process.

It only gives the tax-free allowance for that specific week or month. This is why some employees may notice higher deductions when they are placed on a noncum tax code.

It is not always a mistake. Sometimes it is used because HMRC needs more information before issuing the correct cumulative code.

Why Might Someone Be Put on a Noncum Tax Code?

A person might be placed on a noncum tax code when HMRC or the employer does not have enough information about their current or previous income.

It is often linked to emergency tax treatment, but it can also happen in other situations.

Starting a New Job Without a P45

One of the most common reasons is starting a new job without giving the new employer a P45. A P45 shows details of earnings and tax paid in the current tax year from the previous job.

Without it, the new employer may not know how much income the employee has already received or how much tax has already been deducted. In that case, payroll may apply a non-cumulative or emergency tax code.

Returning to Employment After Self-Employment or Unemployment

Someone who has been self-employed, unemployed, or outside regular PAYE employment may also receive a non-cumulative code when starting a job. HMRC may need time to update their records before issuing the correct code.

This can also happen if a person had mixed income during the year, such as freelance work followed by employment.

Having a Second Job or Pension Income

A second job can also lead to a non-cumulative code, especially where the personal allowance is already being used against the main job. HMRC may allocate different tax codes across different sources of income.

For pensioners, a non-cumulative code may appear where pension income changes or where HMRC needs to adjust tax across employment and pension payments.

An employment tax specialist described the situation like this:

“When I review payslips for people with two jobs, I usually check where the personal allowance has been allocated first. I have seen many cases where the second income is taxed differently not because payroll made an error, but because HMRC is trying to prevent the allowance being used twice.”

Can a Noncum Tax Code Cause Someone to Pay Too Much Tax?

Yes, a noncum tax code can cause someone to pay too much tax temporarily. This usually happens when the person has unused personal allowance from earlier in the tax year, but the non-cumulative code does not apply it.

For example, if someone starts a job in September after not working since April, they may have several months of unused personal allowance.

A cumulative code may recognise this and reduce the amount of tax deducted. A non-cumulative code may only apply one month’s allowance, which can result in higher tax deductions.

However, overpaid tax is not always lost. Once HMRC updates the person’s tax code, the payroll system may correct it through future wages if a cumulative code is issued.

If this does not happen before the end of the tax year, HMRC may calculate the overpayment later and issue a refund where appropriate.

How Long Does a Non-Cumulative Tax Code Usually Last?

A non-cumulative tax code is often temporary, but the length of time can vary. It may last only one pay period if the correct information is supplied quickly.

In other cases, it may remain for several weeks or months until HMRC updates the person’s record.

The timing can depend on:

- Whether the employee provides a P45

- Whether the starter checklist is completed correctly

- How quickly HMRC receives and processes payroll information

- Whether the person has more than one job or pension

- Whether there are previous underpayments or adjustments

Employees should not assume the code will correct itself immediately. It is sensible to check the payslip and, where needed, contact payroll or HMRC.

How Can Someone Fix a Noncum Tax Code?

A person can often fix a noncum tax code by making sure HMRC and payroll have the correct employment and income details. The exact step depends on why the code was applied.

Providing a P45 to Payroll

If the employee has recently left another job, they should give their P45 to the new employer as soon as possible. This helps payroll understand the employee’s previous earnings and tax paid in the current tax year.

If the P45 is not available, the employer may ask the employee to complete a starter checklist. This helps determine the correct temporary tax treatment.

Updating Details Through HMRC

Employees can contact HMRC to update their employment details, estimated income, benefits, pension income, or job changes. HMRC can then issue a revised tax code to the employer where needed.

This is especially useful where someone has changed jobs, left a second job, started receiving pension income, or believes their tax code does not match their current situation.

Checking the HMRC App or Personal Tax Account

Many people can check their tax code through the HMRC app or their Personal Tax Account. This allows them to see current employment records, estimated income, and tax code details.

If something looks wrong, the person may be able to update details online or contact HMRC directly.

How Can Someone Claim a Tax Refund After Being on a Noncum Tax Code?

If someone has overpaid tax because of a non-cumulative code, they may receive the money back through payroll once the correct cumulative code is applied. This can happen automatically in a later wage or salary payment.

If the tax year has already ended, HMRC may review the person’s records and send a tax calculation. Where too much tax has been paid, HMRC may issue a refund.

A person can also check their Personal Tax Account to see whether they are due a refund. In some cases, they may be able to claim it directly online.

The important point is that a non-cumulative tax code does not always mean the money is gone permanently. It may simply mean the tax position has not yet been fully balanced.

What Should Employees Check on Their Payslip?

Employees should check their payslip regularly, especially after starting a new job or changing income sources. A tax code can appear small on the payslip, but it can affect take-home pay.

Key details to check include:

- The tax code shown on the payslip

- Whether the code includes W1, M1, or X

- Gross pay before deductions

- PAYE income tax deducted

- National Insurance deductions

- Year-to-date taxable pay

- Year-to-date tax paid

If a person sees a noncum tax code and does not understand why it has been applied, they should first check whether they recently changed jobs, failed to provide a P45, completed a starter checklist, or started a second income.

What Should Employers and Payroll Teams Do About Non-Cumulative Tax Codes?

Employers and payroll teams must usually apply the tax code provided by HMRC or use the correct starter process when a new employee joins. Payroll teams cannot simply choose a preferred tax code without proper instruction.

However, they can help employees understand what the code means and what information may be needed.

Employers should:

- Ask new starters for a P45 where available

- Use the starter checklist when no P45 is provided

- Apply HMRC tax code notices correctly

- Explain payslip codes clearly where possible

- Encourage employees to contact HMRC for personal tax queries

A non-cumulative code may be correct at the time it is applied. The problem often occurs when employees do not know why it is there or what action they can take to update it.

Is a Noncum Tax Code Always a Problem?

A noncum tax code is not always a problem. In many cases, it is a temporary code used to prevent the wrong amount of tax being deducted while HMRC confirms the person’s details.

It may be appropriate when someone has just started a job, has no P45, or has more than one source of income. It can also help prevent someone receiving too much tax-free allowance at once.

However, it should not be ignored. If the code stays on the payslip for several pay periods and the person believes their records are now up to date, they should check with payroll or HMRC.

The key is to understand whether the code is temporary and whether it matches the person’s actual income situation.

Final Thoughts

A noncum tax code means income tax is calculated on a non-cumulative basis, using only the current pay period rather than the full tax year so far.

It is commonly shown as W1 or M1 and is often linked to new jobs, missing P45 forms, second jobs, pension income, or incomplete HMRC records.

Although it can lead to temporary overpayment of tax, it is usually fixable once the correct information is provided.

Employees should check their payslip, provide their P45 where possible, use their HMRC Personal Tax Account, and contact HMRC if their tax code appears incorrect.

For most UK employees, the non-cumulative tax code is not something to panic about. It is a sign that the PAYE system is using a temporary method until the person’s full tax position is clearer.

FAQs About Noncum Tax Code UK

What does noncum mean on a payslip?

Noncum means non-cumulative. It shows that tax is being calculated only on the current pay period rather than the person’s total earnings and tax paid across the tax year so far. It may appear with W1, M1, or a similar marker on the payslip.

Is a non-cumulative tax code the same as emergency tax?

A non-cumulative tax code is often used as part of emergency tax treatment, but the two terms are not always exactly the same. Emergency tax usually applies when HMRC or the employer does not have enough information to issue a final tax code. A non-cumulative basis is one way payroll may calculate the tax temporarily.

Why does a tax code show W1 or M1?

W1 means the tax code is being applied on a week-one basis, while M1 means it is being applied on a month-one basis. Both mean the payroll system is looking only at that pay period rather than the full tax year.

Can someone get a refund after being on a noncum tax code?

Yes, someone may receive a refund if they have paid too much tax while on a noncum tax code. The refund may come through payroll after HMRC issues a corrected cumulative code, or it may be repaid after the tax year ends.

Does a noncum tax code affect personal allowance?

Yes, it can affect how the personal allowance is used during the year. A cumulative code can carry forward unused allowance from earlier pay periods, but a non-cumulative code usually applies only the allowance for the current week or month.

Should an employee contact HMRC or payroll first?

An employee can start by asking payroll whether they have received the correct tax code and whether the P45 or starter checklist has been processed. If the issue relates to personal income details, previous jobs, second jobs, or HMRC records, the employee may need to contact HMRC directly.

Can a second job cause a non-cumulative tax code?

Yes, a second job can lead to a non-cumulative or adjusted tax code. This can happen where the personal allowance is already being used against the main job, so HMRC applies a different tax treatment to the second income.

How can someone check if their tax code is correct?

A person can check their tax code on their payslip, through the HMRC app, or by using their Personal Tax Account. They should compare the code with their current employment, income, benefits, and pension details to see whether anything looks outdated or incorrect.

What is your reaction?