How Much State Pension Will I Get if I Have Never Worked?

What is the UK State Pension and How Does It Work?

The UK State Pension is a regular payment from the government designed to support individuals in retirement. Eligibility depends on National Insurance (NI) contributions or NI credits. There are two versions:

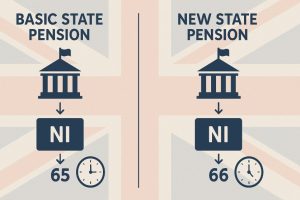

- Basic State Pension: Applies to people who reached retirement age before 6 April 2016

- New State Pension: Applies to those reaching retirement age on or after 6 April 2016

As of the 2025/26 tax year, the full New State Pension is £221.20 per week, amounting to £11,502.40 per year. This amount is reviewed annually and is increased in line with the triple lock system.

To receive the State Pension, individuals must have reached the official State Pension age, which is currently 66 but will rise to 67 by 2028. Further increases are likely in future years based on life expectancy and government review.

Can You Get a State Pension Without Ever Working?

Even if a person has never been employed, it is possible to qualify for the State Pension. Employment is the most common way to earn National Insurance contributions, but the system also recognises non-working circumstances.

Eligibility can be granted through:

- NI credits received while claiming benefits like Carer’s Allowance or Universal Credit

- Claiming Child Benefit for children under the age of 12

- Being a registered carer for someone who is ill, disabled, or elderly

Individuals who never formally entered the workforce, such as stay-at-home parents or long-term caregivers, may meet the minimum requirement through these alternative qualifying routes.

How Many Years of National Insurance Contributions Are Needed?

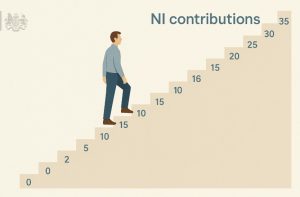

The State Pension system requires a minimum of 10 qualifying years to receive any payment. These years do not need to be consecutive.

To receive the full New State Pension, individuals must have 35 qualifying years of National Insurance contributions or credits.

The value of the weekly pension is proportional to the number of qualifying years between 10 and 35. If someone has 20 qualifying years, they will receive a pension equal to about 20/35ths of the full amount.

Estimated Weekly and Annual State Pension by Qualifying Years:

| Qualifying Years | Weekly Pension Estimate | Annual Pension Estimate |

| 10 years | £63.20 | £3,286.40 |

| 20 years | £126.40 | £6,572.80 |

| 30 years | £189.60 | £9,859.20 |

| 35 years | £221.20 (Full) | £11,502.40 |

The pension is paid every four weeks and is deposited directly into the recipient’s bank account.

What is the Role of National Insurance Credits in Pension Eligibility?

National Insurance credits are essential for individuals who do not work but are involved in qualifying roles such as caregiving.

These credits act as a substitute for paid NI contributions and help protect pension rights during periods of unemployment, illness, or childcare.

Eligibility for NI credits may arise from:

- Receiving Carer’s Allowance or Child Benefit

- Being on Statutory Sick Pay or Jobseeker’s Allowance

- Claiming Employment and Support Allowance

- Being a registered foster carer or full-time carer for at least 20 hours per week

Some credits are awarded automatically, while others require a claim. It is important to verify entitlement with HMRC or the Department for Work and Pensions to ensure that these credits are properly recorded.

How Can Non-Working Individuals Boost Their State Pension?

For individuals who have not worked or have limited employment history, it is still possible to increase their future State Pension entitlement.

The UK government provides several options to help non-working individuals make up for gaps in their National Insurance (NI) record, ensuring they receive as much support as possible during retirement.

One of the most effective ways to boost a State Pension is by filling in NI gaps.

Gaps can occur during periods when a person was not employed, was self-employed but did not earn enough to pay contributions, or was living abroad.

These gaps can reduce the total number of qualifying years, which directly impacts how much State Pension an individual is entitled to.

Making Voluntary National Insurance Contributions

Non-working individuals can make Class 3 voluntary contributions to fill in the years they did not pay or receive NI credits.

These contributions are not compulsory, but they are a strategic choice for anyone nearing retirement age who wishes to secure a larger State Pension.

A few key details about voluntary contributions:

- Class 3 contributions are paid to fill missing years in your NI record

- You can typically go back up to 6 tax years, though temporary extensions sometimes allow further backdating

- Each full year purchased can add up to £316 per year to your State Pension (based on 2025 figures)

- The cost for one year of Class 3 contributions is approximately £907.40 (for the 2025/26 tax year)

Voluntary contributions are usually worthwhile if the increased pension payout exceeds the upfront cost within a few years of retirement.

Before deciding to pay, individuals are encouraged to use the State Pension Forecast tool and consult with HMRC or a financial adviser.

Claiming National Insurance Credits

NI credits can be claimed by individuals who were not working but were in recognised unpaid roles. These credits count toward qualifying years and help maintain eligibility for a full or partial State Pension.

People may qualify for NI credits if they were:

- Claiming Jobseeker’s Allowance or Employment and Support Allowance

- Caring for a child under 12 years old while claiming Child Benefit

- A registered carer or foster parent

- Receiving Carer’s Allowance or caring for at least 20 hours a week

- On Statutory Sick Pay or other qualifying benefits

Some of these credits are applied automatically, especially when individuals claim relevant benefits, but others require a formal application. Checking your NI record regularly ensures all eligible credits are being counted.

Using the State Pension Forecast and NI Record Check

Understanding your State Pension situation is essential before taking steps to boost it. The government offers online tools to help:

- The State Pension Forecast provides a personalised estimate of your pension amount and the number of qualifying years you currently have

- The National Insurance Record service shows your full NI history, highlighting any gaps or incomplete years

These tools are available via GOV.UK and require a Government Gateway account to access. Reviewing this information early allows sufficient time to make adjustments before reaching State Pension age.

Deferring the State Pension to Increase Payments

Another method to increase pension income is deferring the State Pension. If a person chooses to delay claiming their pension once they reach the qualifying age, the amount they receive later can increase.

As of the current rules:

- For every 9 weeks of deferral, the pension increases by 1%

- This equates to roughly 8% extra per year

- Payments are higher once they begin, providing a lifetime increase

This strategy may suit individuals with other sources of income who do not immediately need their State Pension and are in good health with a longer life expectancy.

Applying for Pension Credit if Contributions Cannot Be Increased

For non-working individuals who are unlikely to reach 10 qualifying years or cannot afford voluntary contributions,

Pension Credit is an alternative. It ensures a minimum level of income and can top up other sources of retirement income.

Although Pension Credit does not increase the State Pension itself, it offers financial support and access to additional benefits such as:

- Help with rent or mortgage interest payments

- Council tax reductions

- Cold Weather Payments and free NHS prescriptions

- A free TV licence for those aged 75 and over

Eligibility is based on income and savings, not NI contributions, making it an important safety net for low-income pensioners.

Do Spouses or Partners Who Never Worked Qualify for a Pension?

The Basic State Pension system allowed married individuals to claim based on their partner’s contribution record.

This applied particularly to women who stayed home while their husbands worked. However, under the New State Pension, entitlement is individualised.

A spouse who never worked must now qualify for their pension through their own NI contributions or credits. There are still some limited provisions for inheriting pensions:

- In cases of divorce, individuals may receive credit for the former spouse’s NI record up until the date of divorce

- If the partner is deceased, certain elements of their State Pension may be transferred depending on the age of the surviving spouse and the pension rules in place at the time of their partner’s death

For couples, entitlement is assessed separately, but income from both individuals is considered when determining eligibility for means-tested benefits like Pension Credit.

What is Pension Credit and How Can It Help?

Pension Credit is a means-tested benefit for pensioners with low incomes. It helps bridge the gap for those who may not qualify for the full State Pension, including individuals who have never worked or have insufficient NI contributions.

There are two main elements:

- Guarantee Credit: Tops up weekly income to a minimum threshold

- Savings Credit: Available to those who have made modest savings or contributions towards retirement, but only for people who reached State Pension age before 6 April 2016

Pension Credit Thresholds (2025/26):

| Category | Weekly Income Guarantee |

| Single person | £218.15 |

| Couple | £332.95 |

Pension Credit is often overlooked but can also entitle recipients to additional benefits such as:

- Help with housing costs and council tax

- A free TV licence for those over 75

- Cold Weather Payments during winter months

It is crucial for those who haven’t worked and receive a small or no pension to assess eligibility for Pension Credit, as it can substantially raise their standard of living.

How Do You Claim the State Pension If You’ve Never Worked?

Individuals must actively claim their State Pension; it is not issued automatically.

About four months before reaching the State Pension age, a letter will be sent by the Department for Work and Pensions with instructions.

The application process involves:

- Applying online via GOV.UK, over the phone, or by post

- Providing your National Insurance number

- Submitting identification and bank account details

After the application is approved, payments begin within five weeks and are made every four weeks.

Even for those who have never worked, claiming should not be delayed, especially if they believe they have qualifying years from credits.

It is also possible to defer the State Pension, which can increase the weekly amount once payments begin.

This option should be considered carefully depending on health, finances, and personal circumstances.

How Much Could You Actually Receive Without Working?

The exact amount someone can receive if they’ve never worked will vary depending on how many NI credits they have.

If they’ve qualified for the minimum 10 years through credits, the weekly pension would be approximately £63.20.

With each additional qualifying year, the amount increases proportionally until the full pension rate is reached at 35 years.

Those with less than 10 qualifying years receive no State Pension but may qualify for Pension Credit.

For example:

- A person with 15 qualifying years may receive around £94.80 per week

- A person with 25 qualifying years may receive around £157.20 per week

People with no qualifying years at all will not be entitled to the State Pension but may still receive support through other benefits depending on their circumstances

It is advisable to check with HMRC or use the State Pension forecast service to get an accurate estimate and take corrective action if needed.

Conclusion

While it is possible to receive the State Pension without ever working, the amount you receive will likely be partial, unless you’ve accumulated sufficient NI credits.

The system is designed to support individuals who have been in non-paid roles like caregiving or child-rearing.

It’s essential to check your National Insurance record and understand your entitlements.

Making voluntary contributions, claiming Pension Credit, or accessing NI credits can make a big difference in retirement planning.

FAQs

Can I get a UK State Pension if I’ve always been a stay-at-home parent?

Yes, if you claimed Child Benefit for a child under 12, you may have received National Insurance credits that count towards your State Pension.

What happens to my pension if I was on long-term sickness benefits?

You may have received NI credits through Employment and Support Allowance, which can count toward your State Pension entitlement.

Can carers qualify for State Pension without paying NI?

Yes, carers may receive NI credits if they are eligible for Carer’s Allowance or are registered as a carer for 20 hours or more per week.

Is it worth making voluntary NI contributions in my 60s?

If you’re below State Pension age and have gaps in your NI record, making voluntary contributions can help boost your pension and may be worth considering.

Will Universal Credit help me qualify for a pension later?

Universal Credit itself doesn’t count toward pension eligibility, but some recipients may get NI credits that contribute to their record.

What is the difference between Basic State Pension and New State Pension?

The Basic State Pension applies to those who retired before April 2016. The New State Pension is for those reaching pension age after that date and has different contribution rules.

How do I check how much State Pension I will get?

You can use the official HMRC State Pension Forecast tool on the GOV.UK website to see your estimated pension and identify any NI gaps.

What is your reaction?